Bassett Furniture - Deserving of a Seat at the Table

Originally Published September 5th, 2022

The value finder is back for what hopefully is the lucky number seven edition as we move into Labor Day. The markets may be closed but the research never stops!

What do we have in store today?

How about a company that:

Has a market cap below $200 million

Is priced at ~2x cash

Has doubled revenue since 2012

Has zero long-term debt

Has recently increased its dividend by 14%

If this all sounds like a winner to you then keep reading as we check out Bassett Furniture Industries, Inc. (BSET).

Company Description

“Bassett Furniture Industries, Incorporated engages in the manufacture, marketing, and retail of home furnishings in the United States and internationally. It operates through three segments: Wholesale, Retail company-owned Stores, and Logistical Services. The company engages in the design, manufacture, sourcing, sale, and distribution of furniture products to a network of company-owned retail stores and licensee-owned stores, and independent furniture retailers; and wood and upholstery operations. As of November 27, 2021, it operated a network of 63 company-owned stores and 34 licensee-owned stores. It also provides shipping, and warehousing services to customers in the furniture industry. In addition, the company owns and leases retail store properties; and distributes its products through other multi-line furniture stores, Bassett galleries or design centers, mass merchants, and specialty stores, as well as sells its products online. Bassett Furniture Industries, Incorporated was incorporated in 1902 and is based in Bassett, Virginia.” — Taken from Finviz.com

Basically BSET makes and sells furniture, something that it has now done for over 120 years. The company is one of the most well known around the industry, and from experience, produce quality goods.

A Quick Take

Bassett has had a wild ride over the past few years, reaching as high as $37 dollars in 2017 before dropping below $5 during the pandemic. Now the price has stabilized after a large peak in 2021 to sit at just below $19 a share.

At this price, its seems like it could be an advantageous long term add to the portfolio. Let me tell you why.

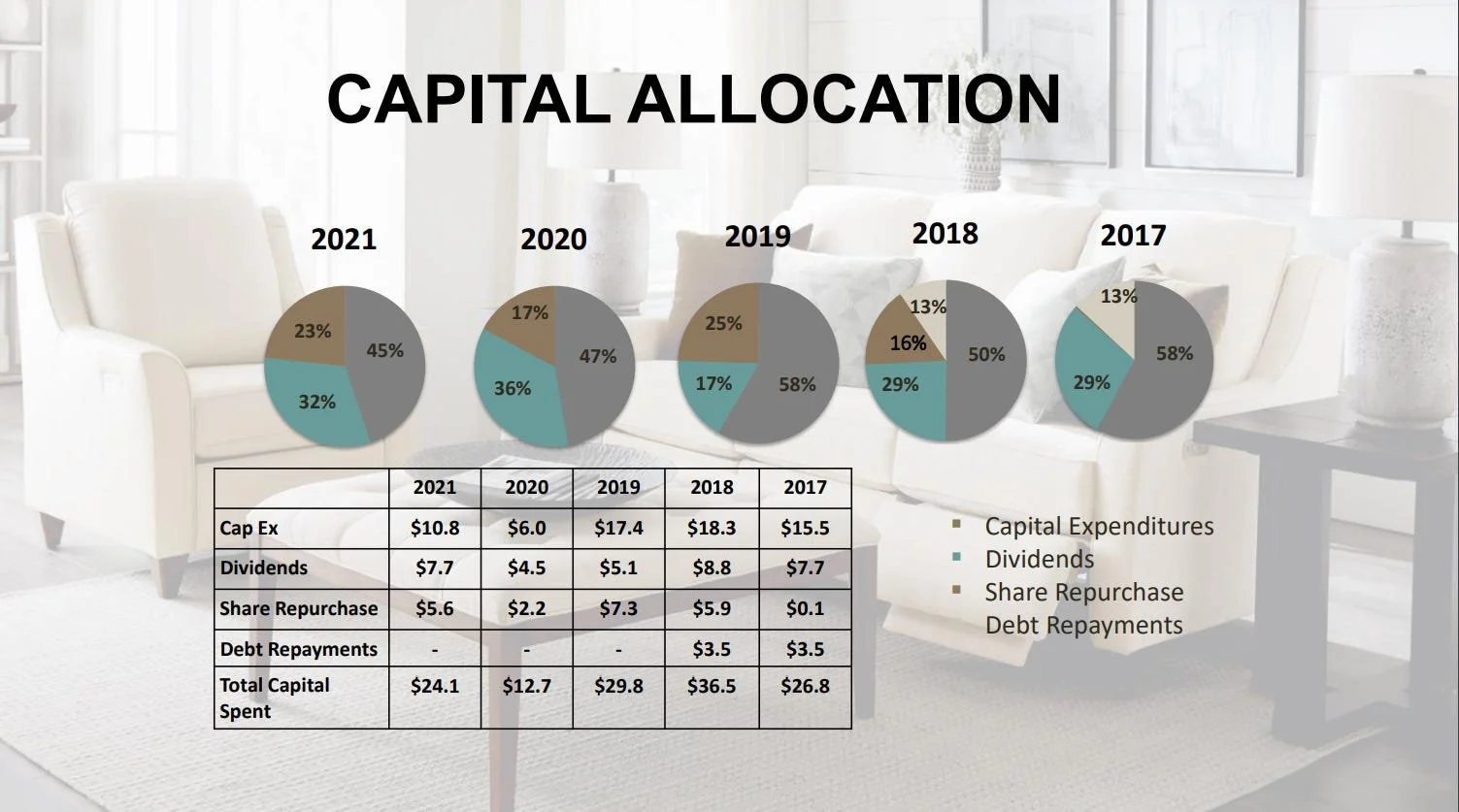

The balance sheet of Bassett is impeccable, with no long term debt, a large amount of cash on hand (~$71 million), and sustainable dividend (~30% payout ratio) that has been raised the past two years in a row. Management has done a tremendous job at being conservative and making sure that they are ready for any worst case scenario that the market could drop on them. They have done all this while also reducing the amount of outstanding shares by almost 10% since 2019.

Returning to the shareholders, while running a consistently profitable business is a strength of this company that seems to have seen it all. They recently paid out a $1.50 special dividend to shareholders during 2022, around an 8% yield on the current price.

—Taken from Bassett’s August 2022 Investor Presentation

So why is the company selling at such low valuations?

Recession risk.

Bassett Furniture falls into the category of consumer discretionary, one that performs poorly when recession hits. During 2009 and 2020, the last two major downturns, Bassett saw revenues decline ~20% both times. Add to this that home sales are beginning to slow and we see some major headwinds to the furniture business.

Here is where it gets interesting though. Bassett’s target population are the upper middle class, in particular upper middle class women. They also have almost 60% of revenue deriving from home sales above $750 thousand dollars in the Southern United States. While this isn’t necessarily recession resistant, it isn’t the crowd that will be pinching every penny to make ends meet or a West Coast software crowd that are seeing massive layoffs.

Taken from Bassett’s August 2022 Investor Presentation

My Final Thoughts

Bassett is a really unsexy, predictable, conservative balance sheet company that really gets my juices flowing. Management has done a tremendous job to set themselves up for future success and they are committed to showing the shareholders love.

The current price ~$19 dollars a share, by my calculations, is sitting pretty much at fair value for the company. This means that while I really like BSET and everything that they have done over the past ten years, I am not quite ready to buy it yet. That being said, I will be adding this to my watchlist to purchase if a recession hits and there is an overreaction in the consumer discretionary industry.

This company is a prime example of what I look for when the market takes a quick downturn. Anywhere around $15 dollars a share, about a 20% drop from its current price, is a slam dunk long-term add for me. To be honest, I am tempted to add some here but really need to stay disciplined as the margin of safety just isn’t there for a downturn.

As always, thanks for reading and happy investing!

The Profit Investigator