Ulta Beauty, Inc. - Making Money with Makeup

Originally Published August 13th, 2022

The year was 2020 and the CoVid-19 pandemic was in full swing. The night was quiet with the exception of a soft rain that fell against the metal roof of my Florida home. Lockdown had been in effect for two weeks now and restlessness was beginning to set in throughout the nation as the appreciation for time at home was now being replaced with the worry of future employment.

My wife and I were spending a significant time at home, between outdoor bike rides and jogs, talking about investing. She had never gotten into stocks or company research but had asked if I could teach her some basics so that she could better understand what I was placing our hard earned money into.

Little did I know that later that week I would learn just as much from her.

As we continued to talk about investing each day, she began to look for some books by female authors in the sector. Many of the books I had recommended, by old gray haired financiers, she felt were boring and disconnected with the normal person.

While searching through various blogs and websites she ran across a book that got her attention. This book was Invested by Danielle Town, a book that I dove into later once she devoured it in less than a week.

One of the main points that she took from it was that she should search out companies with a competitive advantage. Companies that do something better than anyone else and that would be hard to beat in an industry. This had her excited, because she said she instantly knew of one.

She then told me about a company that I had very little clue about.

Photo Credit: Fortune.com

That company was Ulta Beauty, Inc (ULTA).

The more she talked about the brand and the cosmetics that were sold inside the store, the more interested I became. Soon after Florida reopened, we went to the store, that was limiting customers inside, and found a huge line outside the store front.

I didn't go in this time, due to the body limit, but soon I would.

I didn’t necessarily need to go into the store, my wife knows what she is talking about when it comes to this stuff. I trust her with that, as she can rattle off influencer names in the makeup industry, what brands are they are pushing, and which of these are actually quality. She also has an extensive knowledge of each cosmetic store, what they carry, and what they do well or poorly.

My first visit had me intrigued. The store was set up beautifully and there was hustle and bustle all around as people loaded up their bags. Goods that actually ranged in price from what my wife explained as "cheap", "expensive", and "professional". I have no clue about what cosmetics cost, but soon after we went home and began to dig into the financials.

That is when I was all in...

Company Description

Ulta Beauty, Inc. operates as a retailer of beauty products in the United States. The company's stores offer cosmetics, fragrances, skincare and haircare products, bath and body products, and salon styling tools; professional hair products; salon services, including hair, skin, makeup, and brow services; and nail services. It also provides its private label products, such as the Ulta Beauty Collection branded cosmetics, skincare, and bath products, as well as Ulta Beauty branded products; and the Ulta Beauty branded gifts. As of March 10, 2022, the company operated 1,308 retail stores across 50 states. It also distributes its products through its website Ulta.com; and mobile applications. The company was formerly known as Ulta Salon, Cosmetics & Fragrance, Inc. and changed its name to Ulta Beauty, Inc. in January 2017. Ulta Beauty, Inc. was incorporated in 1990 and is based in Bolingbrook, Illinois. --Taken from Finviz.com

There isn't much to add to the description, so we can go ahead and move on.

MOAT

For those unfamiliar with moat, it is the ability for a company to maintain their competitive advantage and fend off competition. This is just like the protection of the medieval moats that were found around castles. I primarily like the description and categories of moat found here by Phil Town of Rule 1 Investing. I won't go into each one here, so I encourage you to read about them if you are unfamiliar.

So what moat does ULTA have?

A major competitive advantage that Ulta has is the Brand. Ulta no doubt has a brand moat that anyone that knows makeup recognizes. It’s a name that is synonymous with both quality and quantity. It’s a name that is known as both a quick stop and a store to get lost in as you browse the immensity of the item selection.

Add to that, the multiple partnerships that Ulta has with various designers/influencer brands and the moat actually may be multi-leveled to include a toll bridge moat. If you want certain brands, you have to go to Ulta. Either way, the moat is strong, with a high gross margin and a low need for Cap Ex.

PROS/CONS

Pros:

The Balance Sheet. First, how about we start with no debt. The biggest factor to ULTAs substantial balance sheet is its continued ability to carry no long term debt. Ulta has continued to be able to develop the company through reinvestment of their own cash flow, rather than borrowing. This should give extreme confidence going forward as many companies will be scrambling with higher rates. Second, I want to note stock based compensation. Always a contentious point when looking at shareholder returns is how a company delves out stock based compensation. Ulta has been very consistent, with compensation being around 4% of net income. This is encouraging as it provides me with a consistent base as I work through valuations and encourages those inside the company to build profitability. Finally, let's talk about the buybacks. In the first quarter, Ulta repurchased 332,000 shares at a cost of $132.8 million. At the end of the quarter, they had $1.87 billion remaining under their current $2 billion repurchase authorization. This is absolutely outstanding.

Photo Credit: Just Jared

Brands. While makeup is a quality game, no question, the other part of the game is the brands that are carried by certain stores, especially those that are endorsed by influencers/celebrities, ie: The Kardashians. Let’s talk about Ulta’s brands for a second. While a company like Sephora offers around 340 brands of makeup, Ulta carries around 600. Ulta is setting up as the new age department store of cosmetics, with items available for all price points and customers. New brands like Fenty Beauty, REM Beauty by Ariana Grande, and Treslúce, a mass cosmetics brand founded by Latin Musician, Becky G, contributed to growth last quarter. While new product launches from a wide range of brands, including Clinique, Lancome, NARS, e.l.f. and NYX also delivered strong sales growth.

Growth. One of the advantages that Ulta has shown in the industry is a tremendous reward program, something that reminds me of the early days of Starbucks (SBUX). Ulta's Ultimate Rewards members now are at 37 million, whereas Starbucks had 24 million in July 2021. If Ulta can continue to find ways to capitalize on these accounts, with 95% of purchases made by Rewards members, it could be a huge growth factor. Another point of growth has been the actual brick and mortar editions. Ulta opened 44 new stores, relocated 7, remodeled 9 last year, while also launching a Wellness shop on Ulta.com, partnered with Target for 100+ locations, added same day delivery in some markets. All of these should continue to drive the earnings growth.

Cons:

Taken from Ulta Investor Presentation 4/2022

Inflation & Recession. This is a double whammy type of environment for companies like Ulta Beauty. While I expect that cosmetics will continue to be strong even in a tough environment, the issues that could occur would be less in the form of revenue and more in the form of margins. Ulta mainly sells three types of cosmetics, Prestige, Mass-tige, and Mass, with the last being the cheapest. If inflation drives up the price of mass products does Ulta lose customers? Likewise, if we head into a recessionary environment, do prestige customers shift purchases to mass or mass-tige products? This is a question that needs to be taken seriously as it will have effects on revenue.

Excess Inventory. The easiest way to start the conversation on this is to take some quotes from the Q1 Transcript:

Total inventory increased 16% to $1.57 billion, compared to $1.35 billion last year. In addition to the impact of 28 additional stores, the increase reflects inventory purchases to support key brand launches, as well as continued efforts to maintain strong in-stocks of key items to support expected demand and mitigate anticipated global supply chain disruptions. Capital expenditures were $71.1 million for the quarter, compared to $34.6 million last year.

So, again, it's up 16% year-over-year. We feel like we're in a good position. Again, it looks easy based on the results we're posting here, but our teams are doing an excellent job and working really hard with our vendor partners, the merchants, the inventory planning teams, the supply chain teams to make sure we get the right product in the right place. And so fill rates are good. We're feeling better. Things have kind of bounced back a little bit from what we saw mid to late last year. So, again, focused on high velocity SKUs, new brands to make sure we take advantage where we can there. We do expect that the growth rate, again, will moderate as we get further into the year this year and start anniversarying some of the steps we took last year to get more aggressive on inventory. So, again, that's one place we always feel confident that we would make more investment if good judgment suggests that. -- Scott Settersten, CFO

Why is the excess inventory a concern? Well if a recession or a switch in customer behavior due to a changing economic environment then Ulta may be sitting on increased inventory that they have to sell at a discount. Did management overshoot the potential future disruptions and expected demand or did they make the right call? We will find that out in time.

New Investments. Just recently an news article was released about Ulta's digital innovation fund (find it here), a new venture that will help fund emerging technology to improve the in and out of store experience. This though, is just one part of the new wave of Ulta investments. Recently Ulta launched UB Media, a retail media network to help promote and connect the brands to customers. These though, have been just the tip of the iceberg as Ulta continues into the tech space.

CEO Dave Kimball spoke about the most recent launches in their Q1 call:

Taken from Ulta.com

We also launched two Virtual Try-On tools, each powered by technology developed by companies we’ve invested in through our digital innovation fund. First, we launched GLAMlab skin advisor 2.0, powered by global artificial intelligence startup, pot.ai . This best-in-class skin analysis technology enables us to provide guests with a more accurate skin diagnosis, which has resulted in stronger satisfaction with the tool. We also launched GLAMlab hairstyle try-on powered by RE/STYLE, a beauty tech start-up that uses artificial intelligence and machine learning to enable virtual try-on of more than 50 different hair styles, including options by gender and texture. We also introduced innovative AR and virtual reality experiences to support our launch of Fenty Beauty and R.E.M. Beauty.

While I love technology, and see the developments as potential growth factors as well as even more of a reason that people will flock to the company, the concern is that Ulta will misuse money to go down a rabbit hole they don't need to. Don't get me wrong, innovation is important and can keep companies from falling from grace, but can also lead to R&D that never shows returns.

Valuation

Now I have my own method of valuing companies, much like those that write these articles. Valuations, no matter how you do them, always take a certain amount of speculation, whether it is organic growth, acquisitions, future debt refinancing, changes to the landscape of the industry, effects of inflation, etc.

The main goal of the valuation process though:

Find a Company that will return 15-20% over the next 5 years.

So how do we do this?

By finding their valuation and buying them at a discount.

When performing valuation estimates of a company's value like Ulta, I like to look at them in through three different lenses. These lenses are:

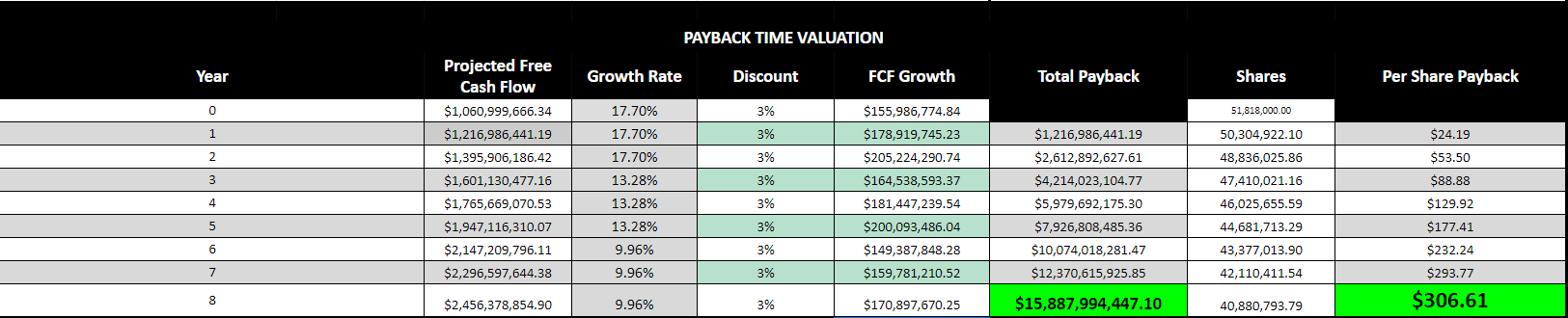

Free Cash Flow Valuation (8 years)

Earnings per share Valuation (5 years)

Free Cash Flow per Share Valuation (5 years)

Let’s begin with the Free Cash Flow Valuation. This equation is based off of the payback rate of free cash flow, which in my equation is simply operating cash flow minus maintenance capital expenditures combined with growth and discount rates. I also like to reduce the total long term debt from the final payback number and follow a the historical rate of stock buybacks or dilution.

I use an 8-year timeline instead of the 10-year seen used by most others. Why is this? Well, I stole this one from Phil Town as well, where he speaks about the payback time that private equity investors expect. He literally wrote a book about this, (here) so instead of me wading through it, I suggest you take a look at his explanation. This, again, leaves me more conservative than most.

Here’s the equation:

The discount rate that I typically use is a steady 3%, until the 10 year treasury yield shows me otherwise (2.84% at time of writing). The growth rate I determine based on a number of factors. I typically use a combination of short term (4-5 yr) historical rates of change, such as Book Value, Sales per Share, FCF per Share, and EPS, as well as a few of others. Then I decide whether I see them as realistic and make adjustments as needed.

While I don’t necessarily maintain that the FCF will end up changing at exactly these numbers, it comes out to an average of just over 10% which I think is a fair estimate.

As you can see, I am paid back significantly less than the current price of the stock. This isn’t the end all be all though, as I still have two more equations to work through until I can make my final judgement call.

Now let’s move to the earnings per share valuation. This equation I like to use because it not only looks at the EPS of the company but also how the market typically values companies in the particular industry and how the company in question has been valued historically.

The EPS history of Ulta is relatively consistent, with the exception of 2020, and I don’t see it changing anytime soon. I will use the average of the growth rates I calculated for FCF and set the EPS growth at 10.65%. I also will use the median P/E over the past 5 years, which comes in just above 27. This isn’t necessarily perfect, but nothing is.

Here is how the calculation lays out:

With the goal in mind of doubling my money every 5 years, aka a 14.4% annual return, I cut the potential future price in half to reach my fair price to purchase the stock. This now leads me on to my final equation.

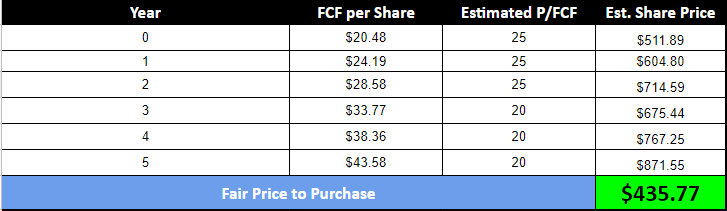

My final equation works off free cash flow per share, a variation of our first equation. The one difference between the two equations though is that I will value the company based off of the historical rates of price to free cash flow.

With Ulta the price to free cash flow over a ten year period has been a bit all over the place, ranging from 54 to 11. The industry median is right around 12, but Ulta is a different beast in the industry and most likely will be treated as such. I decided to go with a starting point of 25, which is just about the average for the past four years.

This equation, like the EPS equation, shows a company that is moderately undervalued, but let’s get to the actual valuation.

My Valuation & Buy Price

So taking all of our newly acquired information, I now move on to the important part, finding what price I actually want to acquire stock at to make the returns I am searching for. This can be found below.

As you can see, the current price is just not enough to get me to the annualized return that I want to see in a five year span. This means that I must use some deductive reasoning to get to a price that I am comfortable with. This price is different for everyone, and really depends on the margin of safety needed due to he understanding of the company. The harder the company is to predict, the more margin that will be needed.

My Current Buy Price = Add anytime Ulta is under $345

Conclusion

While Ulta is a leader in the cosmetic space that I believe will continue to grow its market share and grasp on the industry, it is still facing many near term headwinds. The additional risk of recession, the potential squeeze of margins, and the possibility of customers moving out of the prestige line, means that earnings could see some stagnation.

I do own it in the portfolio, and while I will not sell it at its current price (basically at my fair value), it would have to see revenue perfection to get me over my annual return rates. This is simply not a reasonable risk to take right now and I will continue to patiently wait for the price to come down a bit further before I add more.

Thanks for reading and as always, Happy Investing.

The Profit Investigator