StoneCo Ltd. - The Brazilian Money Machine

Originally Published August 29th, 2022

Let’s get right to the highlights of this week’s find:

Priced right around Book Value

Priced at ~2x Cash

Berskshire Hathaway was an early investor

The third point may have given too big of a hint as to what company the article is featuring today. If you guess StoneCo Ltd. (STNE) then you are correct.

What is StoneCo Ltd. ?

“StoneCo is the fourth largest electronic payments provider in Brazil and helps small and medium-sized businesses (SMBs) enable electronic payments. Their mission is to be the “best financial operating system” for Brazilian merchants in addition to being the “best workflow tool” for merchants, helping them sell more products through their channels.” —Taken from gurufocus.com

To explain it a bit more, StoneCo is a company that works in two different spaces: Financial services and Software. The financial services revenue relies on payment solutions, banking, and a credit product (we will get into that later) and with the software division relying on services that help connect businesses with customers and manage their actual point of sale/ecommerce.

Think an integrated payment solution that also, if the software is used, help companies track inventory, perform point of sale transactions, and basically everything needed to run an ecommerce business.

Or if you want to go way out on a limb, think a Brazilian version of Square.

Sounds pretty good right? Well they have hit some snags recently and the stock has dropped like a stone (pun intended).

What happened?

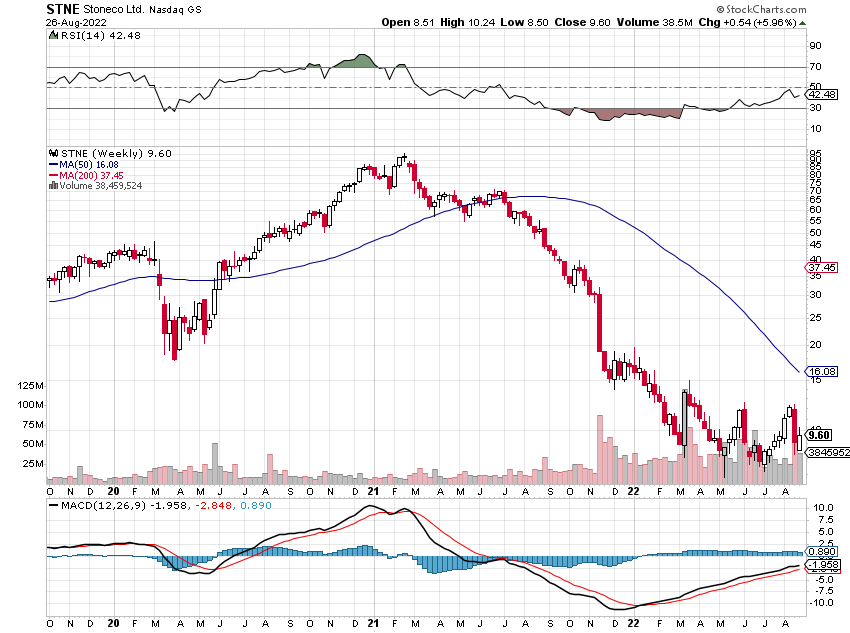

First go ahead and check out the weekly chart.

As you can see StoneCo stock has had a rough time since the beginning of 2021. Why? Well there are multiple factors, including the general turn away from the tech space, but StoneCo’s woes have a much more distinct reason than general market sentiment.

StoneCo started to have some issues in Q2 of 2021 when a huge part of their business going forward, the credit solutions, fell flat on its face. What investors were expecting to be a growth driver became a thorn in its side due to mismanagement of and an environment that exposed the ineptness of those making the decisions. One of the main differentiators of a company like StoneCo is the ability to provide not only banking options but working capital to the small and medium sized businesses it works with.

These bad decisions led to a huge earnings miss, and loss, as well as a guidance of little to zero growth for Q3. This has turned the market sour and dumped the price of the stock.

The Good

What is good about StoneCo?

Well if you remove the missteps in the credit market, and focus on the rest of the business, you will see that StoneCo actually produced pretty solid results. Total payment volumes were up considerably YoY and the payments client base almost doubled from Q2 2021 (1046 to 2066).

Software revenue has also increased, ~23%, YoY, and total revenue has increased over 100% (not over 200%) during that same time frame, when adjusting for the revenue decreases due to the credit-division defaults in 2021.

What now?

Like I said before, StoneCo guided to a zero growth third quarter as the company has turned to be less of an aggressive growth driver to a conservative pessimist when projecting forward growth.

This is a potential opportunity for investors.

With growing payment volumes and a growing client base, as well as a conservative approach to the credit roll out it seems that the company may be trying too hard to place a target that it can’t miss.

The guidance of for Q3 revenues of 2.4 Billion BRL (~$500 million dollars) is roughly a 60% growth from 2021 but expects little to zero growth from the latest quarter that showed solid trajectory. Also, according to the company’s latest earnings call, it is currently testing its working capital products on a small scale and will soon be implementing a pilot program for its credit card products. This means that not only the guidance could be an easy meet/beat but the their could be significant positive news coming out of the credit department at that could have investors again excited about the future.

With all of this information I will probably begin to add StoneCo this quarter as the market continues to fall out of love. With even a high single digit revenue growth over the long term, which I think is super conservative, the current price of STNE to me seems very advantageous.

As always, thanks for reading and happy investing!

The Profit Investigator