GoPro Inc. - Recording Value with Subscriptions

Originally Published October 18th, 2022

It’s another Monday which means it’s time to take a look under the hood of another stock that has fallen out of love with the market. Here at 2k we take pride in zigging when the market zags and this week we have a perfect type of position.

Here is a snapshot:

Forward P/E of 5.57

Price to Cash of 2.53

Price to Sales of 0.69

Short Ratio of 5.42

Debt/Equity of 0.24

What type of company would have these types of ratios? Surely it’s in the industrial or energy sector right?

Wrong. How about a tech company that is a real value play?

Let me introduce you to a familiar name, GoPro Inc. (GPRO).

Company Description

GoPro is a well known company that produces and sells cameras, accessories, and subscription services/software. Most know the company from the action sports cameras that many a Red Bull or extreme athlete has made popular on their YouTube channel doing some crazy stunts.

They have evolved though.

MOAT

On every potential long term investment it is important to look for a competitive advantage, otherwise known as a moat. GoPro is no exception here, and finding a moat isn’t necessarily hard to find. Part of their moat is the brand, as they are extremely well known and in the action camera game it is numero uno. It is the second half of the moat that has been a recent addition and could be the most important. This addition is a switching moat.

A switching moat is one where it is difficult for the customer to switch to another service. GoPro has created this with their newest software and subscription service that we will dig into later.

Pros:

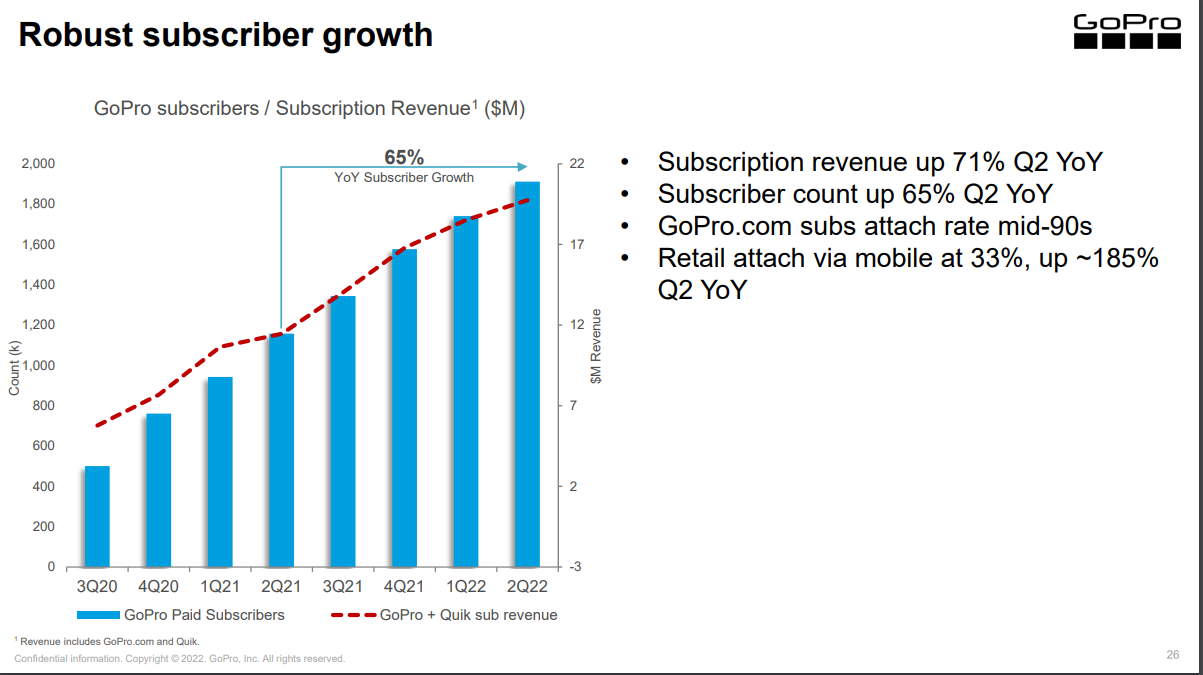

Subscription Revenue. If you want to turn around a company now a days then add an SAAS revenue stream to it. This is precisely what GoPro has done. They added a cloud storage/editing/sharing application that can be purchased by a customer for $49.99 per year. This comes with unlimited storage, discounts on hardware (sneaky), and a very easy to use editing program. Currently GoPro has almost 2 million users, which is up almost 70% from last year and up astronomically from ~250k in 2019. They also offer a mobile only app that allows you to edit and upload videos from your phone (no GoPro hardware needed) for $9.99 a year. This mobile app currently boast around 270k users and GoPro has plans of launching a desktop editing software in 2023. With subscription service sitting at only 6% of total revenue, but at an 70-80% margin, its easy to see how this strength has helped to turn the company profitable.

Debt. You all know that I am a stickler for a balance sheet and debt gets into the way pretty quickly when returning cash to the shareholders. GoPro has done a really nice job over the past couple of years of paying down debt and currently it stands at only $140 million dollars with $38 million in long term lease agreements. With over $200 million dollars in cash and equivalents the company has positioned themselves to survive any type of short term issues that may occur in the market.

Buybacks. Oh buybacks, the magic maker of per share ratios. Have an issue with earnings growth? Then buyback some shares and drive it up artificially! But seriously the thing that I love about GoPro is that they approved a $100 million dollar buyback plan then acted on it aggressively in 2022 while the stock has taken a beating. They continue to drive this narrative, with $78 million left in the program, and I expect them to run through that plan fairly quickly as we head into a recessionary environment.

Cons:

A niche industry. How many action sports enthusiasts that love filming and editing video do you know? Yeah me either. While I know that GoPro hardware is used by some bloggers, fisherman, and even real estate brokers, this market seems to me to be somewhat a niche that may never be large enough to be a massive winner. At an $800 million dollar current market cap it is hard to believe that the $1.2 billion dollars in revenue goes 10x over the next 10 years without a significant catalyst. The hardware still produces most of the revenue and it will be a long ride for the subscriptions to catch up.

Stock based compensation. Remember buybacks that we talked about earlier? Well meet their ugly stepsister stock based compensation. There isn’t much to love as an investor about diluting shares by handing out free stock to your executives as it literally costs you money. In the first half of 2022 the company has provided $20 million dollars in compensation while buying back a total of $22 million in stock. So basically the buybacks have cancelled out the compensations, but that’s not exactly what I was thinking when I was trying to generate more cash flow per share. While some of these are based on merit, it is hard to see what is warranting this much of a bonus.

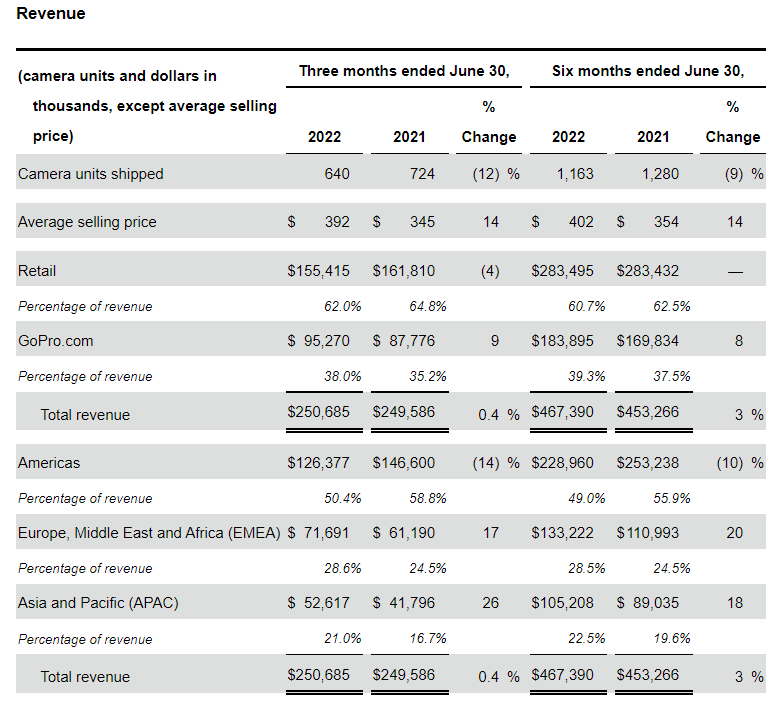

Stagnant Hardware Revenue. GoPro hardware growth was once a driver of the stock price and the earnings. That is now a thing of a long lost past that resembles a fossilized mammoth tusk in a Montana riverbed. Now the company has been developing new cameras that are designed to capture a ever growing social media crowd, but with phones as advanced as we have now who needs to add a $400-$900 dollar camera to the arsenal? For the start of 2022 the company is actually slightly behind on camera units shipped and margins have been slightly decreased due to the inflationary environment that is affecting everyone. This is less than ideal and needs to take a turn for GoPro to realize its true potential.

Conclusion

GoPro is an old name with a new strategy, and that strategy I believe in. The newest cameras are one thing, with features that should help promote to a different audience than the whitewater rafter that smashes it into river rocks, the subscription business though is what strikes my interest. With almost 2 million users of the service GoPro has shown extraordinary growth after making a pivot in how they expect to drive revenue. Add to this a company that has been slowly diversifying its revenue locations, gaining steam in Europe and Asia, and I like what I am seeing.

The company currently sells at just over $5 per share, with $2 of cash per share and producing around $1 of free cash flow per share. This immediately places me into a position where I have some safety heading into a tough environment. The company typically sees large spikes in Q4 due to the holiday, has recently released new cameras that should drive sales during this time, and are near lows for the year.

My valuation for the company places it at a significant long term discount if they can display even minimal growth going forward. I will most likely take a position in GoPro in the next couple of weeks at around 0.5-1% of my portfolio. There is a lot of work still to do for the company but the trajectory seems to be there for me to take a swing at the current price point.

As always thanks for reading, and happy investing!

The Profit Investigator