Turtle Beach: Q3 Report & Conference Call

While there are some writers that are currently making bull or bear cases for the Turtle Beach Corporation (HEAR) I simply wanted to make some notes public that I took while reading, listening, and finally wading through their most recent third quarter results and subsequent conference call.

A couple of points that I think need to be made to all investors first:

I am long a small position in Turtle Beach.

If you are looking to get my actual analysis of the company, you can find it here.

Do your own research no matter what you read on this or any other investing site.

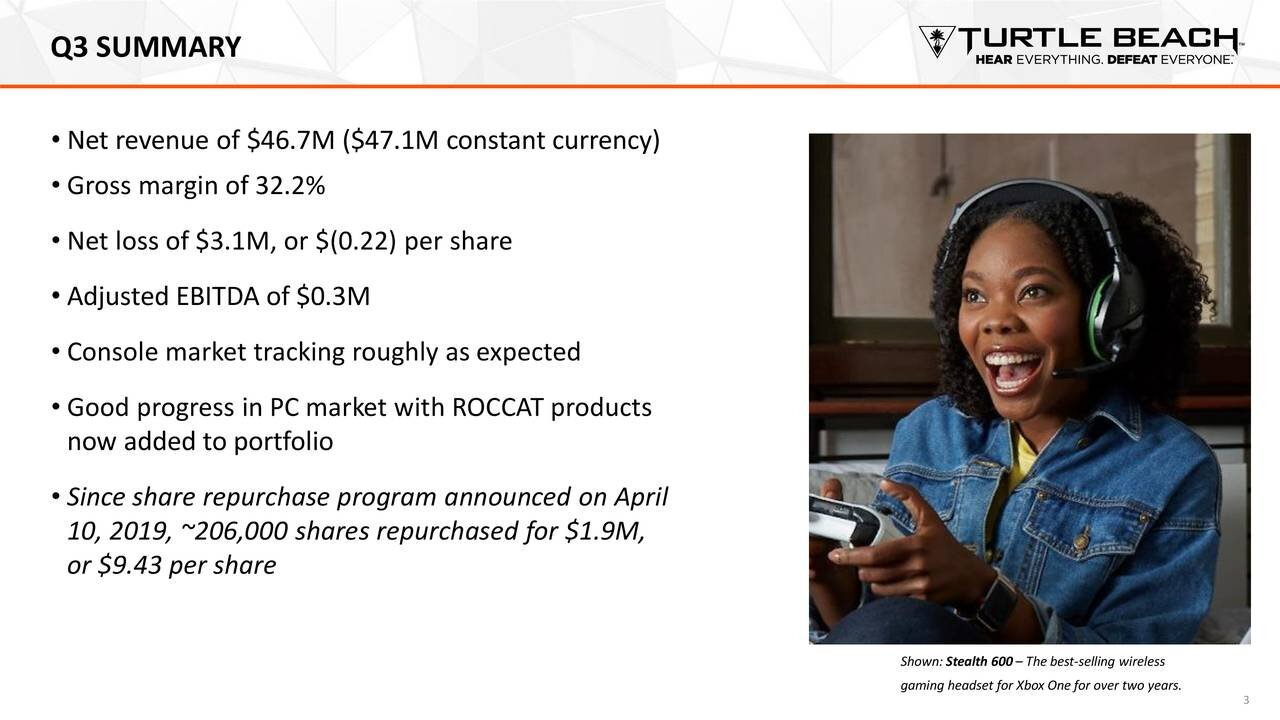

Taken from Turtle Beach Corporation’s Earning Presentation

Okay, so now that I got all of that out of the way let’s jump into the 3rd Quarter report.

There is no way to say it, except that the report did not look great at first glance. At second glance it didn’t look great either, and finally if you went through a third time you may have found some things that brought you out of despair.

What are these things?

Let me start by saying that if you thought 2019 was going to be anywhere remotely near 2018 then I would suggest you owning another stock. The company has already noted multiple times about the influx of unusual business in 2018 and that this year would not look the same. If you missed that, then you really need to research companies further before you invest.

When we take out what looks like to be an anomaly in 2018, and focus on the growth from 2017 until now, you will see a couple of things that really stand out. First, revenue, after revised guidance, should have around a 60% increase. Second, this is coupled with an almost 400% increase in free cash flow. . Third, gross margin of the product shows at around 32% and the company believes that it should remain around the 30-32% mark. Add this to the fact that the company carries no long term debt (they smartly paid that down during the 2018 surplus) and the company has made some major strides over the past two years.

Another point that the company made was that they were updating guidance to include the impact of potential US tariffs on Chinese goods and also noted that they were working to diversify outside of China. This, long term, could be an advantageous move even if the trade deal does get reconciled.

The guidance given by the company disappointed many of the bulls that were expecting huge numbers, but for me was about what I expected to see. The revenue estimate of 236-242 million, the EPS of .65-.75, and the ROCCAT guidance are not things that should scare people but should simply give a clearer picture as to the trajectory of the company during 2019.

The company currently carries a market cap of around 130 million dollars, or just over half of the estimated revenue. At the low end of guidance, this company projects to produce roughly 10 million dollars in net profit which means we may well be currently sitting at slightly undervalued or even a fair price point in this market. If the company is correct that we will see growth in the 2020-2022 markets of 10-15% annually, then this company is a hold at this current price.

The company has also reportedly bought back 206,000 shares since April, at an average of $9.43, which represents only $1.9 million of the proposed $15 million buyback program. I expect to see continued buybacks during Q4 of 2019, most likely at a more accelerated rate if the stock continues to be sold off due to the guidance. Even at a $9.43 price point, we see that HEAR has the ability to reduce their float by around 9% if they do use all $15 million dollars.

Turtle Beach is not a company that will skyrocket in growth like they saw in 2018, but instead should be thought as a slow methodical climber that will continue to produce free cash flow. The addition of ROCCAT is going to be a slow integration into what should be a solid addition to the revenue stream, one that will not be completed until around 2020-2021. Currently the company is projecting 2019 at around a $16-20 million dollar revenue range, which is at the bottom end of the original estimate. The company is still projecting the HEAR PC revenue to be around $100 million in 2021 which I do believe is both conservative and attainable, but obviously remains to be seen as the roll out progresses.

CONCLUSION

I think the biggest things to remember about HEAR is that this isn’t going to be 2018, slow and steady growth is okay, and the guidance was, in my opinion, very conservative. With no long term debt, an entry into PC peripherals, and a large share of the console market I don’t look at this as a company that will be run off by other competitors or even challenged by the “big guys” entering the market. The market cap of HEAR lends itself much more to being acquired by a larger company, which is what I would expect to happen at some point in the near future.